Tag: complexity

-

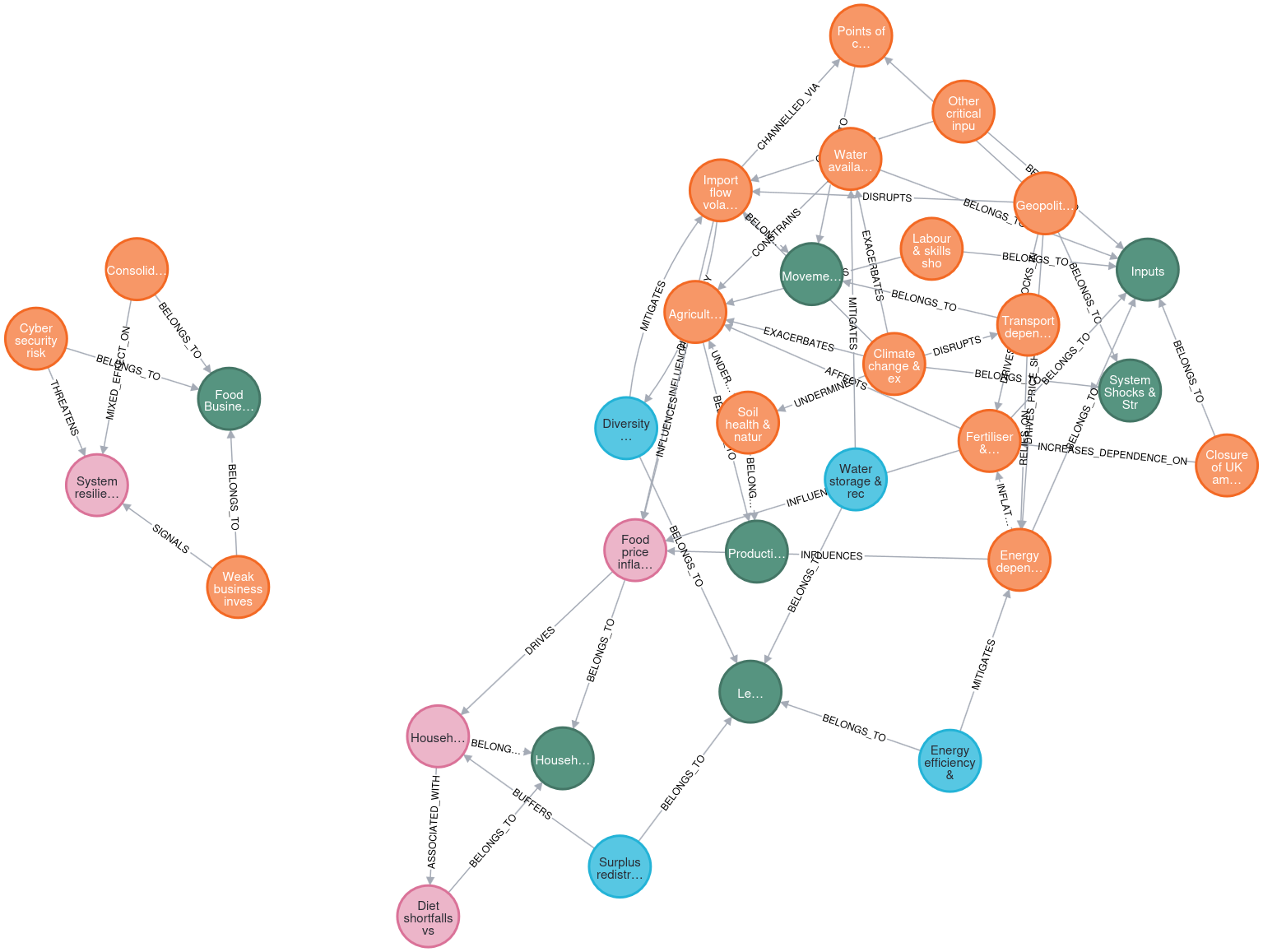

Using AI for systemic risks in food systems

I have long had an interest in systemic risks and failure. How a system can come apart and fail is at last as interesting as how they work, and applying complex systems methods to understand how systems are vulnerable to failure is something I would like to spend more time on. With that in mind…

-

Complexity and the collapse of the financial system – from the Archive

Originally Posted on January 14, 2015 by Institute of Hazard, Risk and Resilience by Philip Garnett and Brett Cherry Finance influences everything, from the growth of businesses and employment to capital and even public services. As the world becomes increasingly subject to the all-encompassing influence of financialisation, it is confronted with problems that require new perspectives from studies in complex systems.…

-

Total Systemic Failure?

My new paper, “Total Systemic Failure?”, is out (this link should get you a free copy for a limited time). I wanted to write something that was more a big picture look at how the world is working. Or perhaps how it isn’t working. I think there is a problem that the world is stuck…

-

The ‘System’ vs Donald Trump

I have been thinking about what Donald Trump means for the ‘system’, by system I am thinking about the complex system that is the US Government Machine and its associated parts. Part of my thinking is that systems of Government have learnt how to persist, they have adaptive to promote and maintain their own existence.…

-

RGS Panel: Risk and Complexity in Finance and Beyond

Our Royal Geographical Society panel, “Risk and Complexity in Finance and Beyond” has been accepted for this years RGS annual conference! Some details below: Session organiser/s: Philip Garnett, The University of York, UK; John H. Morris, Durham University, UK Session chair/s: Philip Garnett, The University of York, UK; John H. Morris, Durham University, UK Session…

-

Complex Beyond Regulation – Global Policy Journal Event

I gave a talk on the 18th of June for a event co-hosted by the Global Policy Journal and Durham University. The title of the talk was “Complex Beyond Regulation”, and its major theme was that the global financial system is now so complex that it is beyond our skill to regulate. I took this…